Asset Classification and Provisioning Norms

The prudent guidelines were first issued by RBI in the year 1991 implemented wef 01.04.1992 on recommendations of Narasimham committee covering, income recognition, asset classification and provisioning. Prudential norms prescribed by RBI include norms relating to Accounting, Exposure, and Capital Adequacy. Prudential accounting norms are income recognition, asset classification and provisioning.

CLASSIFICATION AS NPA

Term Loan : If Interest and/ or instalment of principal remain overdue for a period of more than 90 days

CC/Credit/overdraft : If the account remains ‘out of order or the limit is not renewed/reviewed within180 days from the due date of renewal. Out of order means an account where (i) the balance is continuously more than the sanctioned limit or drawing power OR (ii) where as on the date of Balance Sheet, there is no credit in the account continuously for 90 days or credit is less than interest debited OR (iii) where stock statement not received for 3 months or more.

Bills : If the bill remains overdue for a period of more than 90 days from due date .

Agricultural accounts : (I) if loan has been granted for short duration crop: interest and/or instalment of principal remains overdue for two crop seasons beyond the due date. (ii) if loan has been granted for long duration crop: interest and/or instalment of principal remains overdue for one crop season beyond due date.

Loan against FD, NSC, KVP, LIP : Advances against term deposits, NSCs eligible for surrender, IVPs, KVPs and life policies not treated as NPAs provided sufficient margin is available. Advances against gold ornaments, govt securities and all other securities are not covered by this exemption

Loan guaranteed by Government : Loan guaranteed by Central Govt not treated as NPA for asset classification and provisioning till the Government repudiates its guarantee when invoked. Treated as NPA for income recognition. Advances guaranteed by the State Government classified as NPA as in other cases

Consortium Advances : Asset classification of accounts under consortium should be based on the record of recovery of the individual member banks.

DISTRESSED ASSETS

- Identify incipient stress by creating a sub-category viz., Special mention accounts (SMA) before a loan Account turns into an NPA.

- Early formation of lender’s committee with timeline to agree a plan of resolution.

- Incentives for lenders to agree collectively and quickly to plan.

- Improvement in current restructuring process.

- More expensive future borrowing for borrowers who do not co-operate with lenders.

- More liberal regulatory treatment of asset sales.

Special Mention Account(SMA)-Early Recognition of Stress

- SMA-0 :- Principal or Interest payment not overdue for more than 30 days but account showing signs of incipient stress

- SMA-1 :- Principal or Interest overdue between 31-60 Days

- SMA-2 :- Principal or Interest overdue between 61-90 Days

SMA-0: IDENTIFIED AREAS

- Delay of 90 days or more in

- Submission of stock statement/ other statements such as QOS, HOS and ABS.

- Credit monitoring or financial statements or

- Non renewal of facilities based on audited financials.

- Actual sales/operating profits falling short of projections accepted by 40% or more.

- A single event of non co-operation /prevention from conduct of stock audits.

- Reduction of Drawing Power (DP) by 20% or more after a stock audit.

- Evidence of diversion of funds for unapproved purpose.

- Drop in internal risk rating by 2 or more notches in a single review.

- Return of 3 or more cheques (or electronic debit instructions ) issued by borrowers in 30 days, on grounds of non availability of balance / DP.

- Return of 3 or more bills/cheques discounted or sent under collection.

- Devolvement of Deferred Payment Guarantee (DPG) installments or LCs or invocation of BGs and its non payment within 30 days.

- Third request for extension of time either for creation or perfection of securities or for compliance with any other terms and conditions of sanction.

- Increase in frequency of overdrafts in current accounts.

- The borrower reporting stress in the business and financials.

- Promoter(s) pledging/ selling their shares in the borrower Company due to financial stress

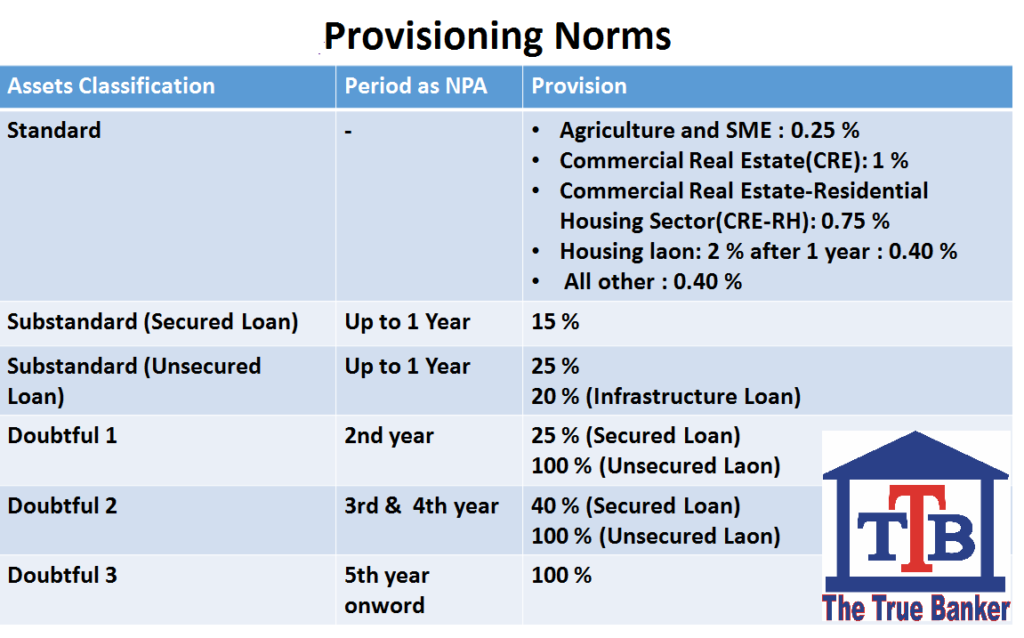

Provisioning Norms